Update: This bill was amended on February 26, 2025 to solely utilize Lodging Sales Tax funds that go to the Montana General Fund. All diversions from the Lodging Facility Use were removed. With this amendment, we no longer oppose this. Our current status is Neutral.

SB90 proposes redirecting funds from the 4%Lodging Facility Use Tax (LFUT) and 4%Lodging Sales Tax to provide residential property tax relief. While we support redirecting funds from the Lodging Sales Tax as this tax is designed to generate revenue for the General Fund—we strongly oppose diverting funds from the Lodging Facility Use Tax, which is essential to sustaining and growing Montana’s visitor economy.

The Lodging Facility Use Tax is the cornerstone of Montana’s visitor economy. This bill eliminates essential programs that fund marketing, preservation, and research that directly drive visitation and spending across the state. These programs are critical to increasing visitor numbers, which in turn generates more Lodging Sales Tax revenue for the Montana General Fund.

The two taxes are intrinsically linked: reducing investment in the Lodging Facility Use Tax will lead to fewer visitors and decreased revenue from both taxes. SB90 threatens to dismantle the programs that sustain Montana’s largest revenue-generating industry by redirecting funds from the Lodging Facility Use Tax. If fewer people visit Montana, both the General Fund and local communities will suffer the consequences of reduced visitor spending.

The Lodging Facility Use Tax is critical to maintaining Montana’s competitive edge in the visitor economy and ensuring the steady growth of the Lodging Sales Tax revenue that benefits the General Fund. Protecting this tax is essential to safeguard Montana’s economic future and the programs and services that support all Montanans.

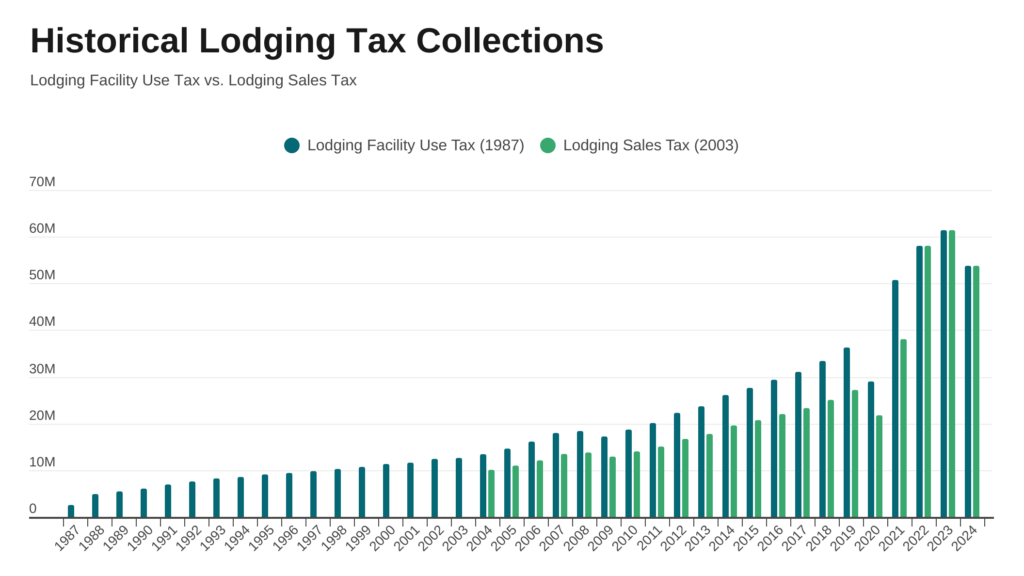

Historical Lodging Tax Collections

Why Investment in the Visitor Economy is Essential

The funding identified in SB90 to be diverted from the Lodging Facility Use Tax supports three programs that sustain and grow Montana’s visitor economy, which is vital to the state’s economic health. These programs include:

Montana Department of Commerce – Visitor Marketing:

A strong visitor economy does not simply "happen"; it is the result of deliberate planning, strategic investment, and ongoing efforts to ensure its growth and sustainability.

Funds initiatives that promote Montana as a world-class destination, encouraging visitors to explore the state during non-peak seasons and across all regions.

Invests in efforts to enhance Made in Montana products, Main Street programs, signage, trade office support, agritourism, and building community resiliency.

Drives visitor spending, which fuels local economies and increases lodging tax revenues for both.

Montana Heritage Preservation:

Protects and promotes Montana’s cultural, historical, and natural assets, attracting visitors and encouraging longer stays.

University System – Institute for Tourism and Recreation Research (ITRR):

Provides a comprehensive range of critical data far beyond marketing trends, offering invaluable insights into various facets of tourism and recreation, including visitor behavior and economic impacts.

Guides businesses and policymakers in making informed decisions to grow the visitor economy sustainably.

Global Competition

Montana competes with destinations worldwide for visitor dollars. States and countries are aggressively investing in marketing and product development to capture market share. Cutting investment in the Lodging Facility Use Tax would:

Weaken Montana’s competitive edge.

This leads to fewer visitors and less revenue for businesses and the General Fund.

Make it harder for Montana to reclaim market share lost to better-funded competitors.

Economic Impact: Direct and Indirect Spending

Visitor spending drives economic activity across multiple sectors in Montana, directly benefiting businesses and generating significant tax revenue:

Direct Spending Categories: Fuel, groceries, dining, lodging, retail, recreational rentals, guided services, licenses/entrance fees, cultural attractions, bars, breweries, distilleries, and gambling.

Indirect Spending Categories: Banking, insurance, construction, supply chains, agriculture, florists, architects, manufacturing, transportation, auto shops, snow grooming, wineries, payroll services, and medical services.

A Network of Opportunity

The ripple effects of visitor spending extend far beyond direct beneficiaries. A thriving visitor economy:

Creates jobs in sectors ranging from hospitality to construction.

Supports the development of community assets like trails, museums, and historic preservation projects.

Stimulates economic growth in small towns and rural areas.

Why This Matters to Montana Homeowners

The visitor economy benefits Montana residents by reducing local tax burdens, creating jobs, and enhancing community amenities. Diverting funds from the Lodging Facility Use Tax risks undermining these benefits:

Tax Revenue Replacement:

Visitor spending generates tax revenue that offsets the need for higher property taxes.

Cutting funding for programs that drive visitation would reduce this revenue, shifting the burden to homeowners.

Job Creation and Income Stability:

Tens of thousands of Montanans work in jobs supported by the visitor economy.

Reduced visitor spending would lead to layoffs, destabilizing household incomes and affecting residents’ ability to pay property taxes.

Community Investments:

Revenue from visitor spending supports local projects—parks, trails, and infrastructure—that enhance the quality of life and property values.

Broader Economic Ripple Effects

A decline in visitor spending would have far-reaching consequences:

Small Businesses: Rural and seasonal businesses rely heavily on visitor spending and would be hardest hit.

Statewide Impact: Reduced spending would lead to lodging tax revenues declining, affecting the General Fund and the programs it supports.

Lost Opportunities: Montana would fall behind competitors in attracting visitors, losing out on billions in potential economic activity.

Historical Lessons

The risks of cutting investment in the visitor economy are well-documented:

Colorado (1993): Eliminating a $12 million tourism promotion budget led to a 30% drop in market share and a $1.4 billion annual revenue loss. Recovery took nearly a decade.

Washington State (2011): Closing the state’s tourism office resulted in a significant decline in visitation and economic activity, requiring costly rebuilding efforts.

Conclusion

Montana’s visitor economy is an intricate system that supports businesses, generates tax revenue, and strengthens communities statewide. Diverting Lodging Facility Use Tax funds would undermine the programs that sustain this system, leading to fewer visitors and less revenue for the General Fund.

We support redirecting Lodging Sales Tax revenue to provide property tax relief, but we oppose diverting funds from the Lodging Facility Use Tax. Preserving the Lodging Facility Use Tax is essential to maintaining Montana’s competitive edge, driving sustainable economic growth, and ensuring vibrant communities for residents and visitors alike.

MONTANA’S TWO LODGING TAXES

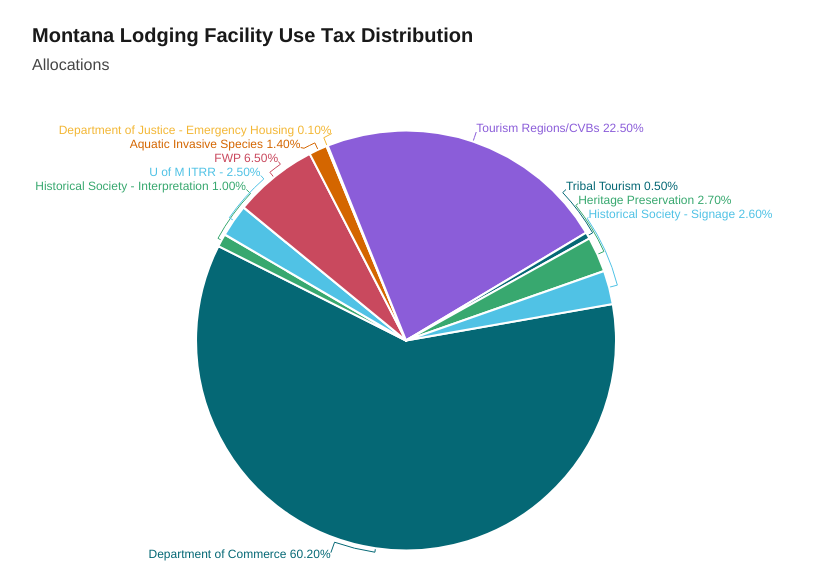

MONTANA'S LODGING FACILITY USE TAX (LFUT), created in 1987 and commonly known as the "bed tax," is a 4% tax levied on guests of hotels, motels, bed and breakfasts, guest ranches, resorts, and campgrounds. The revenue generated from this tax is allocated to various state agencies and programs as follows:

Montana Historical Society: 1% is allocated for installing or maintaining roadside historical signs and historic sites.

Montana University System: 2.5% is designated for the Montana travel research program, the University of Montana Institute for Tourism and Recreation Research (ITRR).

Department of Fish, Wildlife, and Parks: 6.5% is allocated for the maintenance of facilities in state parks that have both resident and nonresident use.

Invasive Species State Special Revenue Account: 1.4% is directed to this account to support efforts in managing aquatic invasive species.

Department of Commerce: 60.2% is used directly by the department for tourism promotion and related activities.

Emergency Lodging for Victims of Domestic Violence or Human Trafficking: 0.1% is allocated to provide emergency lodging for victims.

Regional Nonprofit Tourism Corporations and Convention and Visitor Bureaus (CVBs): 22.5% is distributed among regional nonprofit tourism corporations based on the proceeds collected in each tourism region.

State-Tribal Economic Development Commission: 0.5% is allocated for activities in the Indian tourism region.

Montana Historical Interpretation State Special Revenue Account: 2.6% is designated for historical interpretation projects.

Montana Heritage Preservation and Development Account: 2.7% or $1 million, whichever is less, is allocated to this account, with the Montana Heritage Preservation and Development Commission required to report on the use of these funds semiannually.

These allocations support a wide range of programs and initiatives to promote statewide tourism, preserve Montana's heritage, and maintain state parks and facilities.

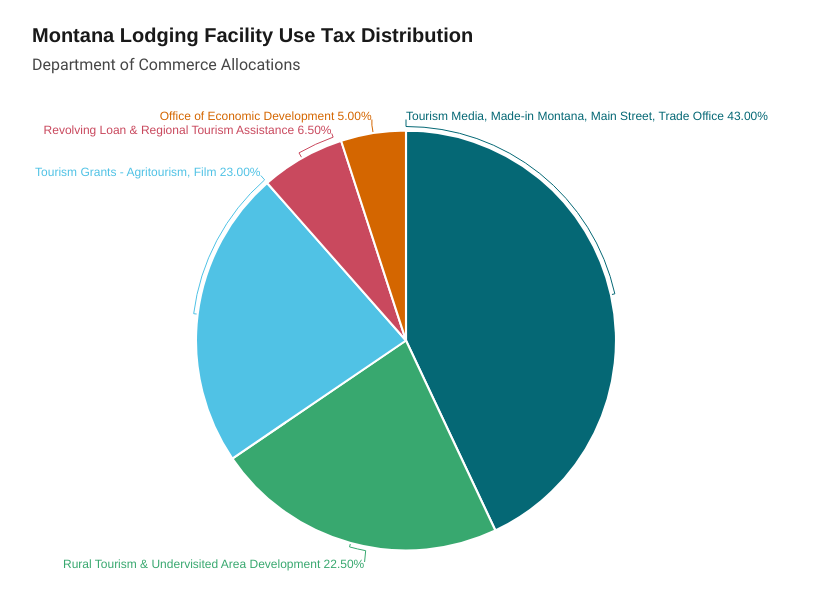

In 2023, the Montana Legislature passed Senate Bill 540, which revised the allocation of the Lodging Facility Use Tax revenue to focus on investing in rural and under-visited communities. The new allocation is as follows:

Tourism Media and Advertising: 43% for tourism media, advertising, film programs, made-in-Montana promotions, main street programs, wayfinding and signage, and support to trade offices.

Rural and Under-Visited Area Projects: 22.5% for rural tourism, under-visited area attraction projects, and tribal tourism, including infrastructure, tourism-related emergency services, marketing, and promotional activities.

Tourism Grants: 23% for tourism grants, including agritourism grants and Montana-based film grants.

Revolving Loan Programs and Regional Tourism Assistance: 6.5% for revolving loan programs and regional tourism assistance.

Collaboration with the Office of Economic Development: 5% for collaboration with the Office of Economic Development for new tourism attractions, other state business development programs, and support for the activities mentioned above.

This shift in funding, as codified under Montana Code Annotated (MCA) 15-65-101,aims to promote and develop tourism in rural and under-visited areas of Montana, moving beyond the focus on national icons like Glacier National Park and Yellowstone National Park prior to 2020.

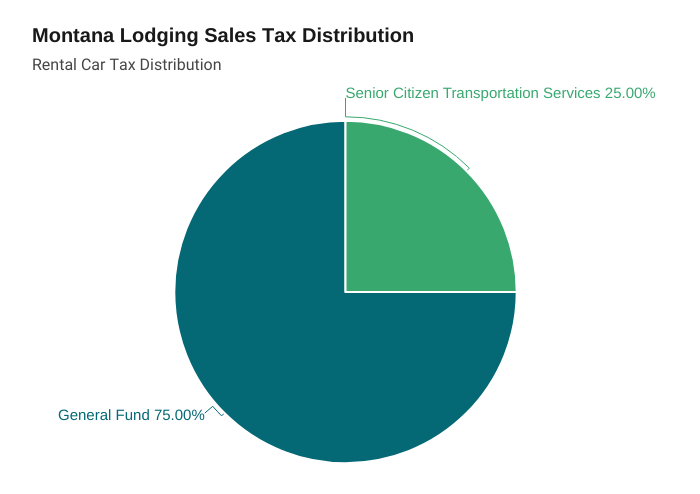

As of January 2025, MONTANA'S LODGING SALES TAX is a 4% tax applied to charges for accommodations such as hotels, motels, campgrounds, resorts, and vacation rentals, alongside an additional 4% tax on the base rental for rental vehicles. Established in 2003, this tax has been a consistent and vital contributor to Montana’s General Fund, supporting essential public services and government operations for over two decades. In recent years, it has also played a transformative role in funding key projects, including the construction of the Montana Heritage Center in Helena, which was completed using Lodging Sales Tax revenue collected between 2020 and 2024. Starting this year, a portion of the tax revenue now funds the center’s ongoing maintenance and operations.

General Fund: 75% of the Lodging Sales Tax revenue and 75% of the Rental Car Sales Tax revenue are allocated to Montana’s general fund, providing long-term financial support for statewide programs and services.

Montana Heritage Center: From 2020 through 2024, 20% of Lodging Sales Tax revenue funded the construction of the Montana Heritage Center. As of 2025, 6% of the revenue is dedicated to the museum's operation and maintenance, ensuring its sustainability as a cultural cornerstone.

Historic Preservation Grants: Another 6% supports the historic preservation grant program, which funds statewide projects to preserve Montana’s heritage.

Capital Developments: 7% of Lodging Sales Tax revenue goes to Montana’s capital developments account, which funds key infrastructure and building projects.

An additional 25% of Rental Car Sales Tax revenue is allocated to the state special revenue fund to support transportation services for senior citizens and individuals with disabilities, addressing critical mobility needs.

Since its inception in 2003, this tax has exemplified Montana’s strategic use of visitor-generated revenue to strengthen public services, preserve its heritage, and invest in critical infrastructure. The allocations, codified in Montana Code Annotated (MCA) 15-68-820, reflect a commitment to fiscal responsibility and statewide impact.

NONRESIDENT VISITOR SPENDING AND TAX REVENUE

Nonresident Visitor Spending in 2023

Based on the most recent data from the Institute for Tourism and Recreation Research (ITRR) for 2023, nonresident visitors to Montana spent approximately $5.45 billion during their trips.

The breakdown of how each visitor dollar was spent is as follows:

Gasoline and Diesel: 23% of total spending, amounting to $1.25 billion, was spent on fuel, reflecting Montana's vast distances and reliance on road travel.

Lodging: 21%, or approximately $1.15 billion, went to accommodations, including hotels (14%), short-term rentals (5%), and campgrounds/RV parks (2%).

Restaurants and Bars: 20%, equating to $1.09 billion, was spent on food and beverages at dining establishments and bars.

Retail Purchases: 15%, or around $820 million, was used for shopping and supporting local businesses and artisans across Montana.

Outfitters and Guides: 10%, or $545 million, was spent on recreational rentals and guided services, highlighting Montana's appeal for outdoor adventures and experiences.

Groceries and Snacks: 6%, approximately $327 million, was spent on groceries and snacks for trips, including self-catering or on-the-go meals.

Licenses and Entrance Fees: About $273 million, or 5%, was allocated to permits, licenses, and entrance fees for parks, cultural attractions, and recreational activities.

This breakdown illustrates how nonresident spending in Montana is distributed across essential and discretionary categories, supporting diverse economic sectors statewide. Fuel, lodging, dining, and retail remain the largest beneficiaries, while outdoor recreation activities, groceries, and fees also contribute significantly to the state economy.

Visitor Spending Generates Tax Revenue

Visitor spending in Montana generates a wide range of tax revenues beyond the lodging taxes that directly fund the money entities, including a significant amount to the Montana General Fund via the LFSUT. When visitors spend money on items such as fuel, groceries, dining, lodging, retail, recreational rentals, guided services, licenses, cultural attractions, and entertainment, they contribute significantly to the state's overall tax base. Here’s how this spending generates various types of tax revenue:

1. Sales and Use Taxes

Fuel Tax: Visitors driving within the state pay fuel taxes, which are earmarked for maintaining and improving Montana’s highway and transportation infrastructure.

Alcohol Taxes: Purchases of liquor, beer, and wine contribute to Montana’s alcohol excise taxes, funding programs such as substance abuse prevention and treatment.

Retail Sales Taxes: While Montana does not have a statewide general sales tax, specific sales taxes, such as for rental vehicles and accommodations, directly fund various state programs and services.

2. Excise and Special Taxes

Gambling Taxes: Spending at casinos, bars, and other gambling establishments generates gambling tax revenue, which is used to support local governments and fund gambling addiction services.

Tobacco Taxes: Visitors who purchase tobacco products contribute to tobacco excise taxes, which fund healthcare programs and other initiatives.

3. Property Taxes

Spending on businesses directly benefiting from tourism, including vacation rentals and lodges, indirectly supports property taxes paid by property owners. These taxes help fund local government services, schools, and community infrastructure.

4. Entrance and Licensing Fees

Parks and Recreational Areas: Entrance fees to state and national parks, as well as licenses for fishing, hunting, and other outdoor activities, provide revenue for conservation, wildlife management, and park maintenance.

Guided Services and Recreational Rentals: Licenses and permits required for outfitting and guiding businesses generate additional revenue, funding outdoor recreation oversight and infrastructure.

5. Income and Payroll Taxes

Employment in Tourism: Visitor spending supports jobs in industries such as hospitality, retail, transportation, and recreation. These jobs generate payroll taxes, including income taxes and Social Security and Medicare contributions.

Indirect Employment Impact: Businesses benefiting from visitor spending create indirect employment in supply chains (e.g., food suppliers for restaurants, equipment providers for outfitters), further expanding payroll tax contributions.

6. Corporate Taxes

Tourism-related businesses such as hotels, restaurants, breweries, and retailers contribute corporate tax revenues based on their earnings, which support state and local budgets.

7. Economic Multiplier Effect

Visitor spending circulates through Montana’s economy as employees and businesses reinvest earnings locally, generating additional taxable transactions and further expanding the tax base.

Visitor spending touches nearly every sector of the economy, providing critical tax revenue supporting public services, infrastructure, and community development across Montana. This underscores the far-reaching economic impact of a thriving visitor economy.

Based on the most recent data from the Institute for Tourism and Recreation Research (ITRR) for 2023, nonresident visitors to Montana spent approximately $5.45 billion during their trips.

The breakdown of how each visitor dollar was spent is as follows:

Gasoline and Diesel: 23% of total spending, amounting to $1.25 billion, was spent on fuel, reflecting Montana's vast distances and reliance on road travel.

Lodging: 21%, or approximately $1.15 billion, went to accommodations, including hotels (14%), short-term rentals (5%), and campgrounds/RV parks (2%).

Restaurants and Bars: 20%, equating to $1.09 billion, was spent on food and beverages at dining establishments and bars.

Retail Purchases: 15%, or around $820 million, was used for shopping and supporting local businesses and artisans across Montana.

Outfitters and Guides: 10%, or $545 million, was spent on recreational rentals and guided services, highlighting Montana's appeal for outdoor adventures and experiences.

Groceries and Snacks: 6%, approximately $327 million, was spent on groceries and snacks for trips, including self-catering or on-the-go meals.

Licenses and Entrance Fees: About $273 million, or 5%, was allocated to permits, licenses, and entrance fees for parks, cultural attractions, and recreational activities.

This breakdown illustrates how nonresident spending in Montana is distributed across essential and discretionary categories, supporting diverse economic sectors statewide. Fuel, lodging, dining, and retail remain the largest beneficiaries, while outdoor recreation activities, groceries, and fees also contribute significantly to the state economy.